Insurance and Your Credit Score: What You Need to Know

Article • 10 minutes

![]() By Matic

By Matic

Your credit score is an important part of your financial picture. It’s used during all kinds of big life moments — like getting approval to rent an apartment, taking out a loan (and determining your interest rate), applying for credit cards, and more. But did you also know that in most US states, your credit score could have a significant impact on your home and auto insurance rates? We’re breaking down the sometimes-confusing topic of how your credit score plays a role in your insurance rates.

How your credit affects your insurance options

Your credit rating impacts what is known as your credit-based insurance score, which is a number used by insurance carriers to determine whether they offer insurance to you and what you pay for it. Your insurance score is different from your credit score, but is calculated using some credit-related factors — like your payment history, credit history length, and any debt you owe. It’s usually based on your credit report from a major credit bureau, like Experian, TransUnion, or Equifax.

Another thing to note is that you won’t have one set insurance score, since each insurance company calculates this number in a slightly different way. Regardless of how your score is calculated, though, one theme carries across the board for most companies — if you have a lower credit-based insurance score, you’ll likely pay more in premiums.

Are you surprised by this information? If so, you’re not alone. In a Matic survey, almost half of all respondents — 45% — did not know that their credit impacts their insurance rates and their ability to get coverage. This finding was even more pronounced for respondents over the age of 60, where 54% said they didn’t know that their credit affected their premiums.*

Did you know that your credit impacts your insurance rates?

Age of respondents who didn’t know that credit impacts insurance rates*

Why do insurance carriers use your credit information?

Insurance carriers can use your credit-based insurance score as one of many elements to come up with your rate and decide whether to offer you a policy. It’s used as a way to predict how likely you are to file a claim (which costs the company money).

What does your credit score have to do with your chances of filing a claim? Some industry research from the Federal Trade Commission shows that people with lower credit scores file more claims than those with good or excellent credit scores — and therefore, your credit history helps insurers predict the level of risk to issue you a policy.

The good news is that your insurance score isn’t the only factor that carriers use to decide the rate they give you — in fact, they’re usually required to use other factors. Learn more about some of the other items that affect your home insurance rates and car insurance rates.

If you have a lower credit score, you might be better off in certain states.

While the majority of US states allow carriers to use credit-based insurance scores, some states have passed laws that restrict the use of credit information by insurance companies. These laws were put in place to allow equal access to insurance, regardless of a person’s financial situation. In theory, if you have a lower credit score, you’d be better off living in one of those states for access to more insurance options for a better price.

However, the states that restrict use of credit information do so to varying degrees — and it can get confusing. For example, a few states allow insurers to use credit in certain cases, like defining your initial rate, but don’t let insurers use credit to increase your rate in the future (like when your policy renews). Others allow insurers to use credit history to decide on rates, but not to deny a policy application or as grounds for a policy cancellation.

According to the NAIC, these eight states have either banned the use of credit information completely or have some limitations on credit use:

Use of credit information is prohibited or significantly restricted

- California

- Hawaii

- Maryland

- Michigan

- Massachusetts

- Nevada

- Oregon

- Utah

Nevada is the latest to join the group of states with credit restriction laws — the state implemented a temporary ban on considering negative credit information from events that happened after March 1, 2020. If the law doesn’t become permanent, the restriction on credit-based insurance scores will expire in May 2024. Additionally, states like Illinois are contemplating measures to address the adverse effects of credit scores on insurance rates, exemplified by the introduction of a bill aimed at banning auto insurers from setting rates based on race, gender, and credit score.

Do credit restriction laws really help?

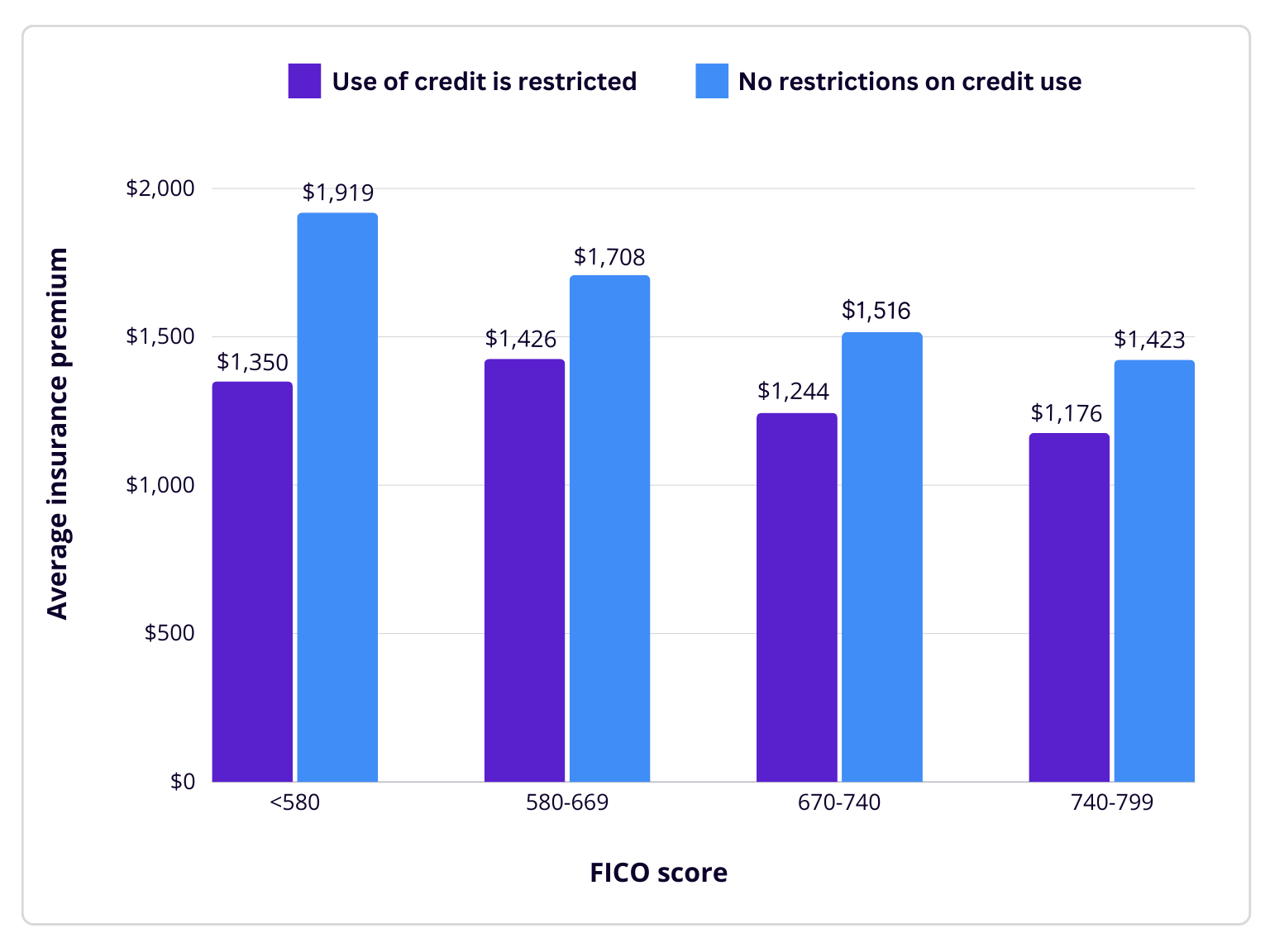

The idea of equal access to insurance for all is great in theory — but are the laws effective? Our data on premiums for home insurance shows that people with lower FICO scores are still paying significantly more, even if they live in a state with restrictions on credit use. According to Matic’s premium data collected between June 1, 2022 and March 1, 2024, people with a FICO score below 580 were still paying $174 more for insurance than those with a score between 740 and 799 in states with credit use restrictions.

Why is this happening? Although insurers can’t use credit information in these states, they can still use your claims history. And as you now know, those with lower credit scores are generally likely to file more claims, and every claim you file negatively impacts your ability to get the best insurance rates.

Chart represents home insurance premium data collected from June 1, 2022 – March 1, 2024

Chart represents home insurance premium data collected from June 1, 2022 – March 1, 2024

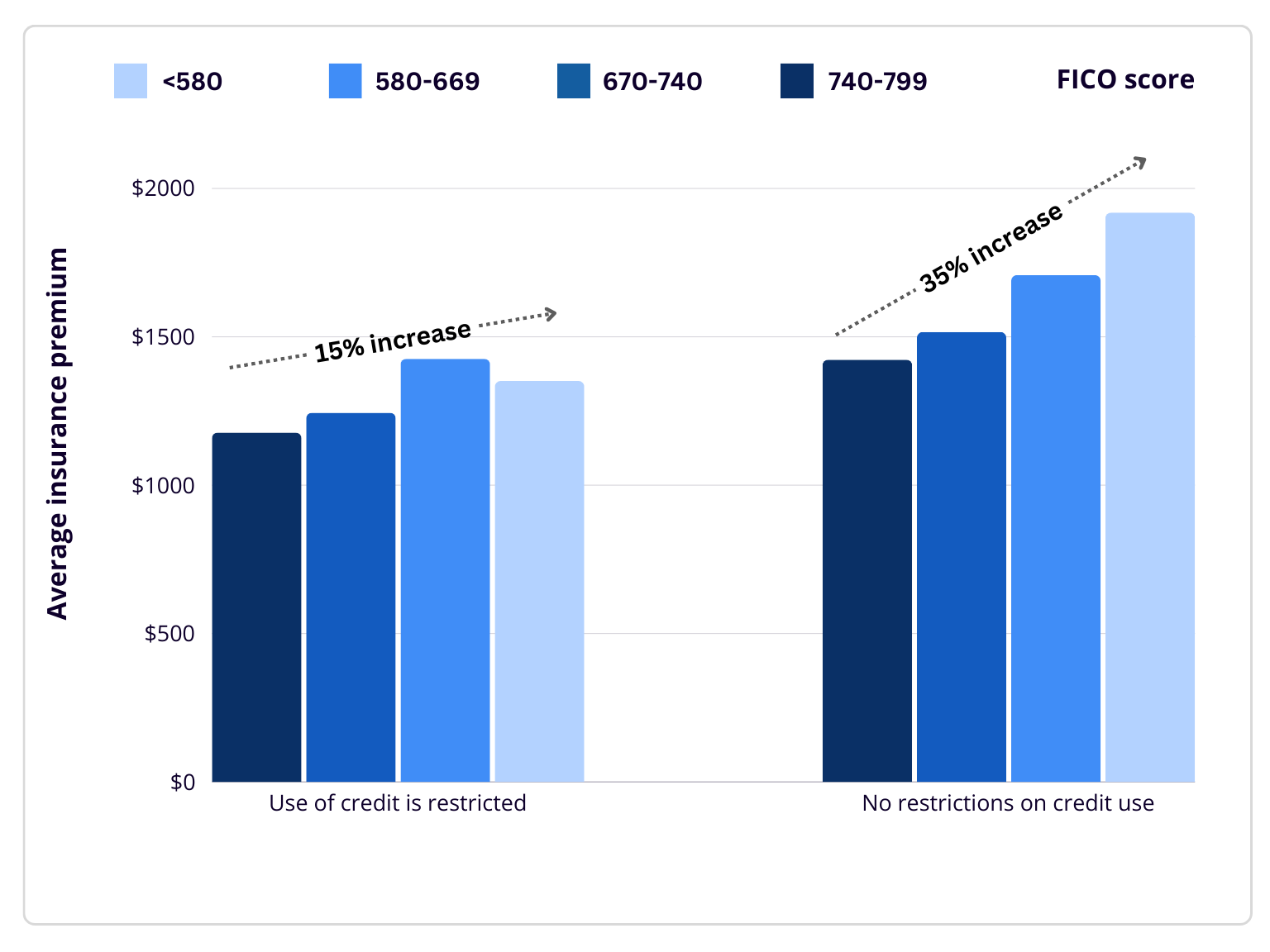

Even if these laws don’t completely eradicate the issue, though, it does appear that people with lower credit scores are better off living in states with restrictions on credit use. For example, if your FICO score is below 580 and you live in a state where credit use is restricted, you’ll pay approximately 15% more in premiums than someone with a FICO score between 740 and 799. While this sounds like a lot, it’s still better than the alternative — you’ll pay a whopping 35% more than those with a score between 740 and 799 if you live in a state with no credit restrictions. In addition, homeowners with a FICO score below 580 are paying 42% more for insurance in states without credit restriction laws compared to people with the same scores in credit-restricted states.

Chart represents home insurance premium data collected from June 1, 2022 – March 1, 2024

Chart represents home insurance premium data collected from June 1, 2022 – March 1, 2024

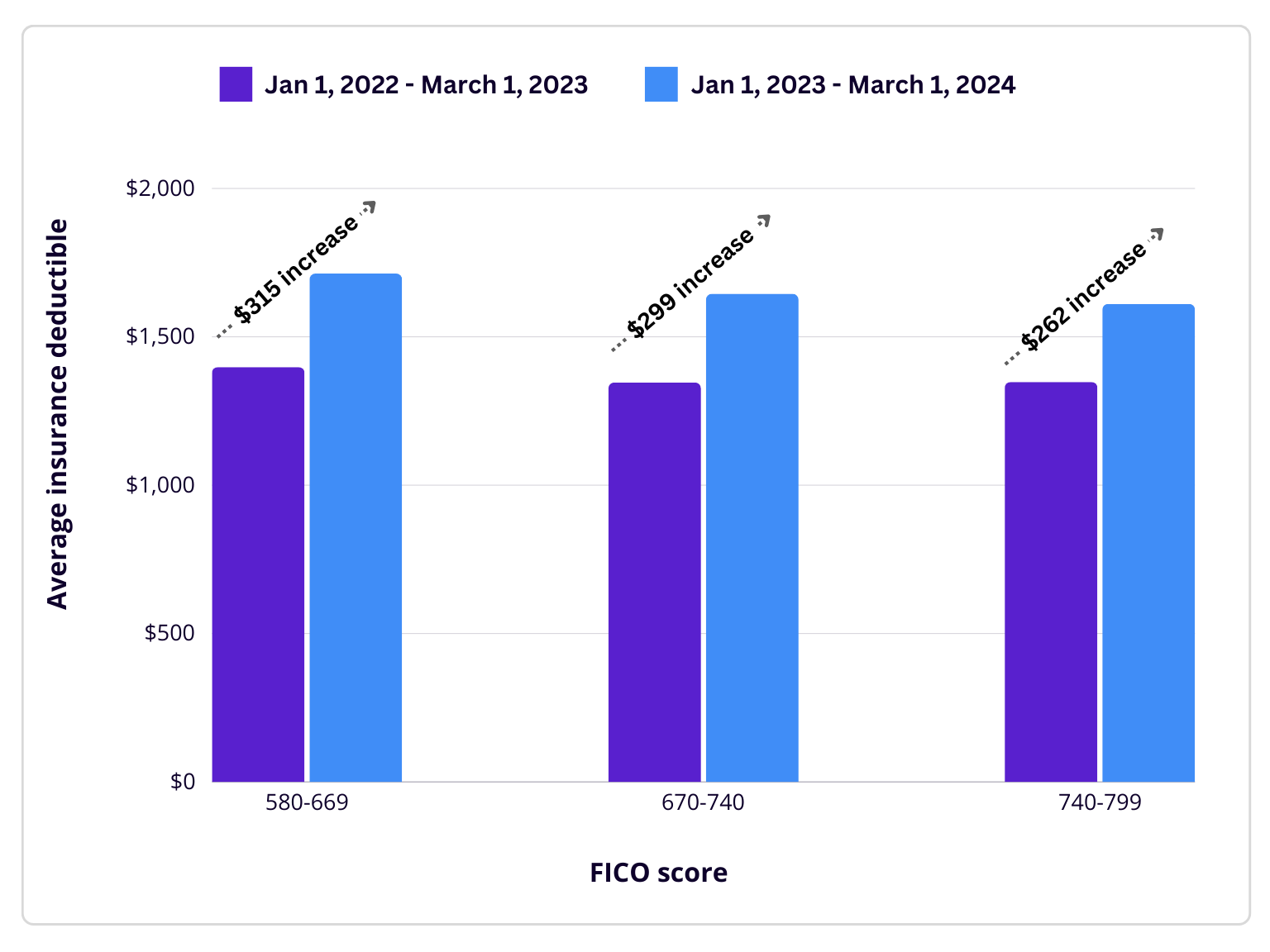

In addition to facing disadvantages in states without credit restriction laws, people with lower FICO scores appear to be taking on more risk with higher deductibles to lower their premiums and save on their monthly escrow payments. For example, homeowners with FICO scores between 580 and 669 had an average deductible of $1,397 from January 2022-March 2023, versus a $1,712 average deductible from January 2023-March 2024 — a $315 increase. Conversely, homeowners with FICO scores between 740 and 799 had a deductible of $1,349 from January 2022-March 2023 and experienced a less severe $262 deductible increase in the following year. The significant increase in deductibles across all FICO categories is largely a result of carriers enforcing or recommending higher deductibles to reduce their losses in a tough insurance market, while some homeowners are self-selecting this route to offset increased premiums.

How to improve your credit score

Now that you know about the importance of your credit score in relation to insurance (for most US states), let’s take a look at a few ways to increase your credit score over time. Improving your credit score will help you secure a home or auto insurance policy and get access to the best rates.

1. Understand your credit score.

Make sure you know your credit score and understand what factors are influencing that score, so you can take steps to improve. You can easily access this information for free from one of the three major credit bureaus.

2. Pay bills on time.

Your payment history is the biggest factor that influences your credit score. One way to combat late payments (if you’ve forgotten to pay your bill on time) is to set up automatic bill payments from your bank account, so you don’t have to keep track of due dates on your own.

3. Keep your credit utilization low.

Credit utilization is the percentage of your available credit that you use each month. If you have access to $20,000 of credit on two credit cards, for example, and you’ve spent $10,000 between the two cards, your credit utilization rate is 50%.

It’s usually recommended to keep your credit utilization rate under 30%. So, if you have access to $20,000 of credit, you shouldn’t use more than $6,000 of it. Why is this? A low credit utilization rate illustrates that you’re managing your finances responsibly and likely not spending above your means.

A few ways to decrease your credit utilization rate include:

- Making fewer purchases with credit cards. If you can pay some of your bills directly through your bank account, consider making the switch.

- Pay your balances in full. If you can’t do this, pay off as much as you can to keep your balance as low as possible.

- Open a new credit card. Getting approved for a new credit card means you’ll have a new line of credit with its own credit limit. This adds to your available credit and therefore, can help lower your credit utilization rate — if you’re careful. Opening a new account doesn’t mean you have more spending power, and it’s easy to overspend with a shiny new card. Plus, opening a new account adds an extra hard inquiry to your credit report (more on this later), which may lower your credit score.

- Ask your credit card issuer for a limit increase. Some credit card companies will bump up your card limit if you simply ask for an increase. This is especially true if your financial situation has changed — for instance, you got a new job that pays more, and are eligible for a higher limit.

4. Don’t close your old accounts.

You might be tempted to close an old credit card that you don’t use, but that could be a mistake. The length of your credit history contributes to your credit score — generally speaking, the longer you’ve had credit available, the better. Plus, if you close an account, you’ll lose access to the available credit on that card, and your credit utilization rate will go up.

5. Avoid hard inquiries, if possible.

Do your best to limit the number of hard inquiries on your credit report. A hard inquiry represents an instance where a new creditor — like a credit card issuer or a lender — has pulled your credit report when you consented for them to do so. If you have many hard inquiries within a short time period (maybe you applied for too many credit cards at once), your credit score may be negatively affected. The good news is that a few hard inquiries over a longer period of time likely won’t have a long-term effect on your score.

Did you know? When you get an insurance quote, you might be concerned that your credit score could plummet from the check on your credit report. This is a myth. While insurance carriers do check your credit report during the quoting process, it’s considered a soft inquiry when they do so. A soft inquiry is simply a check on your credit that doesn’t affect your credit score. Soft inquiries include things like checking your own credit report and getting pre-approved offers from lenders (that you didn’t apply for). Because of this, you can get as many insurance quotes as you want without worrying about your score.

*Survey excluded people living in states where insurance rates are not impacted by credit score.

Looking to save money on insurance?

Matic compares 40+ A-rated carriers to find the right option for you. Get started with a bundled home and auto insurance quote now.

Get a Quote